![]()

Government of India vide Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 on 31.03.2020. notified relief measures related to Income Tax return filings, GST compliance, PAN-Aadhar linkage and other statutory and regulatory issues.

Income Tax Act 1961 also covers under the Specified Act as per Para 2 of the ordinance.

Extension of TDS Return (Q4 ) Filing date

As per Para 3(1)(b) the Ordinance ,where any limit has been specified in specified Act which falls during the period from 20th day of March 2020 to 29th day of June 2020 , for the compliance of –furnishing of any return under the provision of specified Act ,Then the time limit for completion shall stand extended to the 30th of June 2020

Interest for late deposit of Tax deducted for the month of March 2020 : As per Para 3(2) of the said Ordinance :-

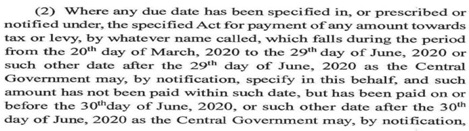

Where any due date has been specified under the specified Act for payment of any amount towards tax which falls during the period from 20th day of March 2020 to 29th day of June 2020 and such amount has not been paid on or before 30th June 2020, then notwithstanding anything contained in this Act:

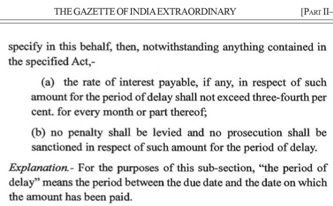

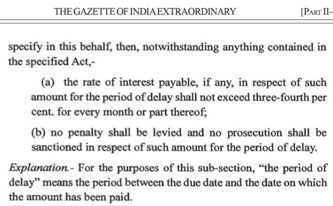

Interest shall be levied in respect of such amount for the period of delay not exceeding three-four percentage (.75%) for every month or part thereof .

The rate of interest payable

However , there will not be any penalty and prosecution in respect of such amount for the period of delay .

Explanation – For the purpose of this sub section the period of delay means the period between the due date and the date on which the amount has been paid

Thus , it is clear that whilst date of TDS filing which is 31st May ( falls between 20 March 2020 – 29 June 2020 )is extended to 30th June 2020 , delay in deposit of TDS will be subject to interest @ .75% for every month of delay .

We are providing training in Labor Laws, Payroll, Salary Structure, PF-ESI Challan, Bonus, TDS-Form 16 & more:

- HR-Generalist-Practical-Training: https://oneclik.in/hr-generalist-practical-training/ (PF, ESI, Bonus, Payroll & more)

- Labour-Law-Practical-Training: https://oneclik.in/labour-law-practical-training/ (Factory, Contact Labor, Maternity Act & more)

- PF – ESI Consultant Service: https://oneclik.in/pf-esi-consultant-service/

To get connected & for latest HR, IR, Labor Law Updates:

- Join our Telegram Channel for Latest HR – IR – Labor Law Updates – Click: “One Clik”

- For Whatsapp Group: https://wa.me/919033016939

- Facebook: One Clik

- Linkedin: One Clik

- Instagram: oneclik_hr_management