![]()

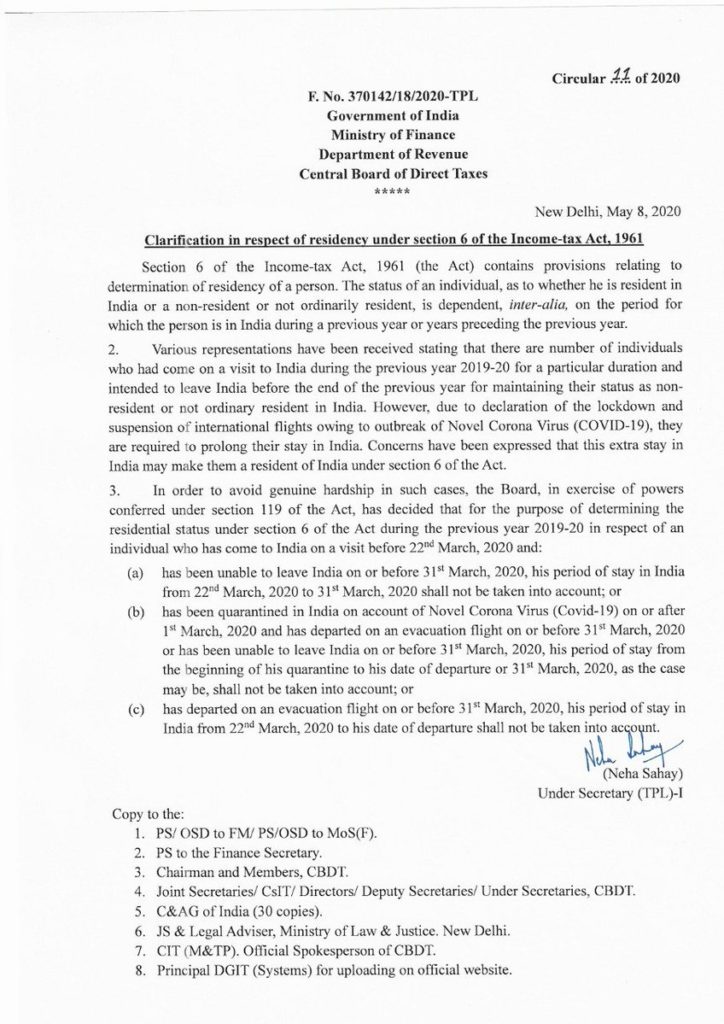

Taking note of the COVID-19 lockdown, the Central Government has granted relaxations to the criteria for determining ‘residential status’ under Section 6 of the Income Tax Act,1961, for the Financial Year 2019-20.

As per Section 6 of Income Tax Act (before 2020 amendment), stay for 182 days or more in India during a financial year will make an individual ‘resident in India’ for the purposes of income tax liability.

Several individuals, who are otherwise non-resident Indians, had to prolong their stay in India on account of the COVID-19 lockdown. Considering various representations seeking relaxations on residency status, the Central Board of Direct Taxes has granted the following relaxations.

For the purpose of determining the residential status under Section 6 of the Act during the previous year 2019-20 in respect of an individual who has come to India on a visit before 22nd March, 2020 and :

- has been unable to leave India on or before 31st March, 2020, his period of stay in India from 22nd March, 2020 to 31st March 2020 shall not be taken into account;

- has been quarantined in India on account of Novel Corona Virus (Covid-19) on or after 1st March, 2020 and has departed on an evacuation flight on or before 21st March 2020 or has been unable to leave India on or before 31st March, 2020, his period of stay from the beginning of his quarantine to his date of departure or 31st March, 2020, as the case may be, shall not be taken into account; or

- has departed on an evacuation flight on or before 31st March, 2020, his period of stay in India from 22nd March, 2020 to his date of departure shall not be taken into account.

The Central Board of Direct Taxes invoked powers under Section 119 of the Income Tax Act for making the above changes.

Circular for determining the residential status in such cases for Financial Year 2020-21 would be issued in due course, depending upon normalisation of/ resumption of international flights, the Income Tax department clarified.test ad 4

The Finance Act 2020 has amended Section 6 to reduce the period of stay in India as 120 days from 182 days for claiming NRI status with effect from FY 2020-2021.

We are providing practical training (Labor Laws, Payroll, Salary Structure, PF-ESI Challan) and Labor Law, Payroll Consultant Service & more:

- HR-Generalist-Practical-Training: https://oneclik.in/hr-generalist-practical-training/ (PF, ESI, Bonus, Payroll & more)

- Labour-Law-Practical-Training: https://oneclik.in/labour-law-practical-training/ (Factory, Contact Labor, Maternity Act & more)

- PF – ESI Consultant Service: https://oneclik.in/pf-esi-consultant-service/

- Labor Law, Compliance & HR – Payroll Management

To get connected & for latest HR, IR, Labor Law Updates:

- Telegram Channel: “One Clik”

- Whatsapp Group: https://wa.me/919033016939

- Facebook: One Clik

- Linkedin: One Clik

- Instagram: oneclik_hr_management